It was a packed week last week for economic news, highlighted by key labor market data and a Fed meeting. When the dust settled, mortgage rates ended the week a little lower.

Employment Report Exceeds Expectations

The closely watched Employment Report released on Friday modestly exceeded expectations. Against a consensus forecast of 450,000, the economy gained 531,000 jobs in October, and revisions added 235,000 jobs to the results for prior months. The gains were broad-based across a wide range of industries, led by the leisure and hospitality sectors.

The unemployment rate declined from 4.8% to 4.6% in September, below the consensus forecast of 4.7%. Average hourly earnings, an indicator of wage growth, were an impressive 4.9% higher than a year ago, up from 4.6% last month, and the highest level since February.

Services Sector Index Jumps to All-Time High

A couple of other significant economic reports released this week from the Institute of Supply Management (ISM) highlighted the negative effects of supply chain disruptions on the manufacturing sector. The national services sector index unexpectedly jumped from 61.9 to a record high of 66.7, while the national manufacturing index was roughly flat at 60.8. Levels above just 50 indicate that the sectors are expanding, and readings above 60 are rare. While both reports were very strong by historical standards, supply chain issues not surprisingly have had a much greater impact on manufacturing companies that need materials to produce goods than on companies providing services such as computer programming or banking.

No Surprises in Fed Meeting Notes

For quite a while, the Fed has done a commendable job of communicating its plans to investors in advance, and once again there were no surprises and little lasting impact from the latest meeting.

According to the Fed meeting statement, it will begin to taper its $120 billion per month of bond purchases by $15 billion per month beginning later this month, which was right in line with expectations. Officials continue to anticipate that inflation will ease from current elevated levels as supply chain disruptions are resolved. Little new guidance was provided to help determine the exact timing of the first federal funds rate hike, which is currently expected to take place near the middle of next year.

Major Economic News Due This Week

Looking ahead, investors will be seeking hints from Fed officials about the timing for future rate hikes and will closely watch Covid case counts around the world, particularly in Europe. Beyond that, the Consumer Price Index (CPI) will be released on Wednesday. CPI is a widely followed monthly inflation indicator that looks at the price changes for a broad range of goods and services. The JOLTS report, which measures job openings and labor turnover rates, will come out on Friday. Mortgage markets will be closed on Thursday in observance of Veterans Day.

Looking ahead, investors will be seeking hints from Fed officials about the timing for future rate hikes and will closely watch Covid case counts around the world, particularly in Europe. Beyond that, the Consumer Price Index (CPI) will be released on Wednesday. CPI is a widely followed monthly inflation indicator that looks at the price changes for a broad range of goods and services. The JOLTS report, which measures job openings and labor turnover rates, will come out on Friday. Mortgage markets will be closed on Thursday in observance of Veterans Day.

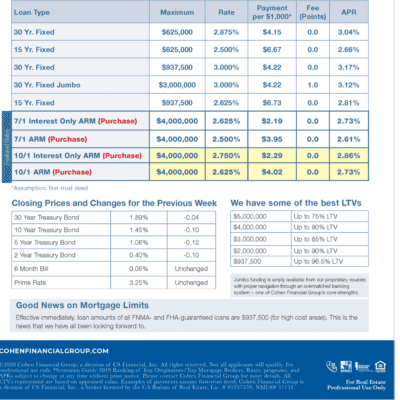

mortgage rates week of 11-8-2021