Despite a stronger than expected report on current inflation, investors appeared to become less concerned about future inflation last week. Combined with a European Central Bank meeting that was viewed as favorable, mortgage rates ended the week a little lower.

CPI Rate of Increase Rises to 29 Yr High

The Consumer Price Index (CPI) is a widely followed monthly inflation report that looks at the price change for goods and services. In May, core CPI, which excludes the volatile food and energy components, jumped 0.7% from April, above the consensus forecast for an increase of just 0.5%. Particularly large increases were seen in prices for used cars and airline tickets. Core CPI was 3.8% higher than a year ago, up from an annual rate of increase of 3.0% last month, and the highest reading since 1992.

The big question is to what degree the pickup in inflation is due to temporary factors or to longer-term influences.

European Central Bank Holds Steady

On last Thursday, the European Central Bank (ECB) made no policy changes, which was the best-case outcome for mortgage rates. The ECB made no mention of a specific time frame for starting to scale back its bond purchase program, and the tone of its meeting statement was relatively dovish. Investors widely expect that its next action will be to tighten monetary policy rather than to loosen it, so holding steady was viewed as positive news.

Labor Market is Tightening

The JOLTS report measures job openings and labor turnover rates, and the latest data indicated that the labor market is tightening. At the end of April, job openings unexpectedly surged to 9.3 million, shattering the former record high. Openings are now more than two million higher than they were in January 2020 prior to the pandemic. A high level of job openings reflects a strong labor market, as companies struggle to hire enough workers. A large number of employees also willingly left their jobs in April. This is viewed as a sign of labor market strength as well since people usually quit only if they expect that they can find better jobs.

The Federal Reserve reported that household net worth at the end of the first quarter of 2021 was 3.8% higher than at the end of 2020. Roughly $3.2 trillion of gains came from stocks and $1.0 trillion was due to increased real estate values.

Major Economic News Due This Week

Looking ahead, investors will continue watching global Covid case counts and vaccine distribution. Beyond that, the next Fed meeting will take place on Wednesday. No change in the federal funds rate is expected, and investors will be looking for more detailed guidance on the pace of future bond purchases. In addition, Retail Sales will be released tomorrow. Since consumer spending accounts for over two-thirds of U.S. economic activity, the retail sales data is a key indicator of the strength of the economy. Housing Starts will come out on Wednesday.

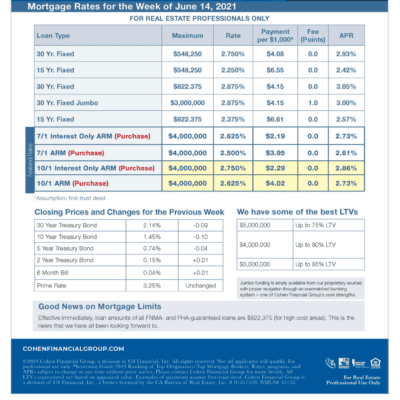

Mortgage Rates Week of June 14