It was another volatile week for mortgage markets, mostly due to the steady stream of headlines about the intensifying conflict in Ukraine. Key testimony from Fed Chair Powell and important labor market data had a much smaller impact. As a result, mortgage rates ended last week lower.

Markets Seek Safety Which is Good for Mortgage Rates

In response to geopolitical events such as the conflict in Ukraine, investors generally seek to reduce the level of risk in their portfolios. Last week, news that indicated greater Russian military action caused investors to shift from stocks to relatively safer assets such as bonds. This increased demand for mortgage-backed securities (MBS), which was favorable for mortgage rates.

Fed Promises First Rate Hike This Month

Last Wednesday, highly anticipated testimony to Congress from Chair Powell helped shape the investor outlook for future Fed policy. While some investors thought that a 50 basis point rate hike was still a possibility, Powell clearly showed support for raising the federal funds rate by 25 basis points at the next meeting on March 16 and expects the action to be followed by a series of additional 25 basis point increases. He did leave open the possibility of larger rate hikes in the future if inflation does not decline at the anticipated pace. In addition, he said that the massive balance sheet holdings of Treasuries and mortgage-backed securities (MBS) will be reduced “in a predictable manner.” Asked about the impact of the conflict in Ukraine on the US economy, he replied that it is “highly uncertain.”

US Job Gains Beats Expectations

The closely watched Employment Report released last Friday revealed strong job gains but weaker than expected wage growth. Against a consensus forecast of 400,000, the economy gained 678,000 jobs in February. The unemployment rate unexpectedly fell from 4.0% to 3.8%. Average hourly earnings were 5.1% higher than a year ago, down from an annual rate of 5.5% last month, and far below the consensus forecast of 5.8%.

Other Data Point to Expansion

A couple of other significant economic indicators released last week from the Institute of Supply Management (ISM) remained at high levels by historical standards. The national lservice sector index came in at 56.5 and the national manufacturing at 58.6. Levels above 50 indicate that the sectors are expanding, and readings above 60 are rare.

Major Economic News Due This Week

Looking ahead, investors will closely follow news on Ukraine and will look for additional Fed guidance on the pace of future rate hikes and balance sheet reduction. Beyond that, the JOLTS report, which measures job openings and labor turnover rates, will come out on Wednesday. The next European Central Bank meeting will take place on Thursday. The Consumer Price Index (CPI) also will be released on Thursday. CPI is a widely followed monthly inflation indicator that looks at the price changes for a broad range of goods and services.

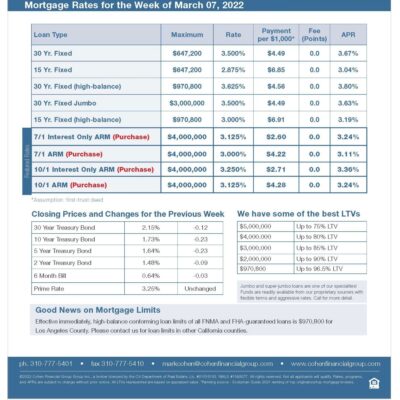

Mortgage Rates Week of 3-7-2022